What We Heard at NCCI’s AIS

The workers’ compensation market is at an inflection point with data confidence. The combined ratio is near a historic low at 91%, among the strongest underwriting results since 2016, and by most measures the market is performing. Yet beneath these favorable results, industry-specific trends are quietly reshaping risk dynamics and future underwriting performance.

For insurers and agents, these shifts reinforce the importance of data-driven underwriting and proactive loss prevention to sustain profitability in an evolving claims environment. Underwriting leaders navigating complex risks increasingly point to data confidence as a defining priority.

Carriers with a trusted data foundation will spot these shifts early and earn the trust of brokers who need a reliable partner. That starts with accurate, complete submission data that underwriting and loss control teams can actually act on.

4 Data-Driven Trends Worth Watching

1. Complex risks are moving into the voluntary market.

More complex workers’ compensation risks are increasingly shifting into the voluntary market. This is raising both growth potential and underwriting pressure as loss severity increases and risk becomes more fragmented across states, industries, and claim types.

In this environment, traditional segmentation is no longer sufficient. Carriers that can combine granular data with predictive analytics to surface emerging loss drivers earlier, at the level of geography, provider behavior, and claim characteristics, will be better positioned to achieve levels of data confidence and maintain underwriting discipline that sustains profitability. The result is more precise underwriting, faster decisions, and stronger portfolio performance.

For workers’ compensation carriers wanting to surface loss drivers early, we’ve learned a trusted underwriting data foundation that enables AI adoption is the best path to achieve deeper analysis and more adaptive decision-making.

We’ve seen this across 50+ implementations, where trusted data at the foundation changes what’s possible across operations. We routinely observe work that used to take days now happens in hours. Carriers are able to respond faster and win more business. And underwriters spend their time on judgment, not data prep. When the data is right, everything else accelerates.

2. State mix and geography are impacting underwriting performance.

In this environment, disciplined risk selection and data-driven underwriting are more critical than ever. Geographic concentration now has a greater impact on loss outcomes, elevating the value of ZIP-code-level insights, provider data, and localized claims trends. This shift underscores the industry’s growing need for data confidence with more precise underwriting intelligence as reflected in ongoing efforts to enhance granular data connectivity and better understand evolving loss drivers.

The geographic variation is also widening, with state-level differences playing a larger role in loss outcomes and underwriting performance. Large losses and tail risk remain persistent concerns, reinforcing the importance of deeper segmentation and early risk identification.

We see this significantly impacting triage, submission prep and loss control. This trend is something we’ve been positioned for and perfected in underwriting production with 5 of the 10 Top Workers’ Compensation carriers.

Insurance Quantified’s intake platform automatically extracts broker submission data in consistent formats, tailored for your underwriting and loss control teams. This surfaces priority submissions to teams easily, because it’s formatted the way you want it, so you can make triage decisions quickly. We expose buried information in loss run and exposure documents critical for submission prep and risk assessment, like high severity claims with a zero dollar loss, but still awaiting litigation or other factors before the final loss is tallied. This superior intelligence also identifies high-risk applicants early for loss control engagement.

3. The underlying risk landscape is changing through the industry.

Employment patterns are shifting, healthcare delivery continues to evolve, and the workforce is aging and changing in composition. As these dynamics reshape claim behavior and loss severity, the actuarial and underwriting assumptions that supported profitability over the past decade may no longer hold as reliably going forward.

Trends show medical severity is increasing at a faster rate while injury frequency is declining, putting upward pressure on overall loss costs despite continued profitability. Trends also highlight medical severity as a key driver of cost escalation, influenced by treatment intensity, provider pricing variation, and evolving care patterns. Data confidence becomes essential when the underlying assumptions are shifting this fast.

This trend will likely continue moving, and it’s why we integrated WCIO-standard classification of body parts and cause of injury into loss run extracts and data summaries. This helps underwriting teams identify high-risk clients early with a comprehensive, data-driven view of the claim and loss severity. We also integrated predictions on workers’ compensation claim subcoverages, helping underwriting teams distinguish between components such as medical and indemnity, providing forward-looking insight into claim outcomes.

4. AI is emerging as a critical tool in workers’ compensation underwriting.

As the workers’ compensation market shifts to a more dynamic and complex underwriting environment, AI is enabling more underwriting capabilities. Carriers are no longer constrained by the availability of data, but by their ability to interpret it fast enough to keep pace with changing loss dynamics.

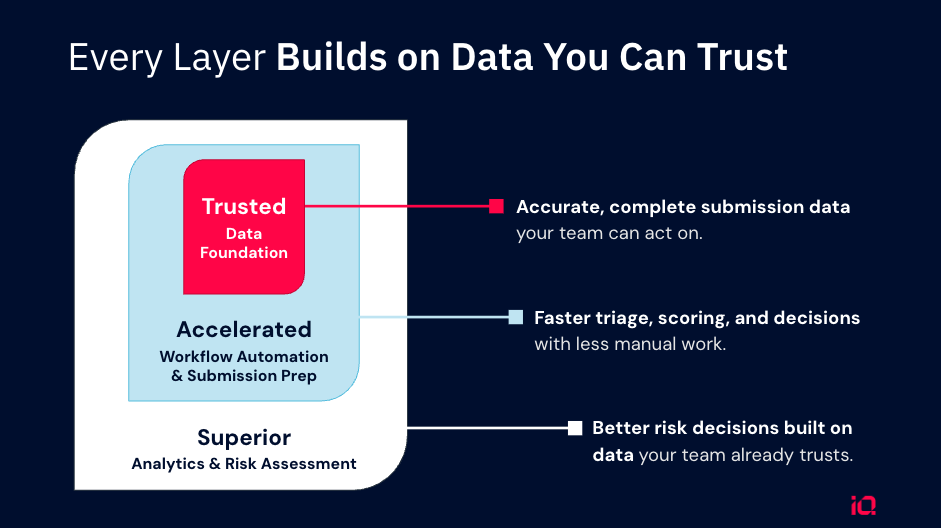

When we talk with workers’ compensation carriers about getting started with AI adoption in their underwriting process, we often hear the struggle is “how” and “where” to start. We recommend starting with a trusted underwriting data foundation that enables AI adoption and fuels their current tech stack. Here’s the 3 layer approach we’ve seen successful across 50+ implementations:

- Layer 1: Automate submission intake to achieve accurate and complete submission data that your teams can act on. When the data is right, everything else accelerates.

- Layer 2: Automate workflow and submission prep to help with faster triage, scoring and decisions with less manual work. Trusted data changes what’s possible across the operation.

- Layer 3: Solidify your trusted data foundation with superior analytics and risk assessment to make better risk decisions built on data your team already trusts.

We’ve seen this enable workers’ compensation carriers convert fragmented data sets into intelligence that helps surface emerging loss drivers earlier, improve segmentation across geography and class, and bring greater consistency to underwriting decisions.

How Insurance Quantified partners with Workers’ Compensation Carriers

Our solutions turns workers’ compensation submissions into decision-ready data, giving your underwriting and loss control teams a reliable foundation they can act on with confidence.

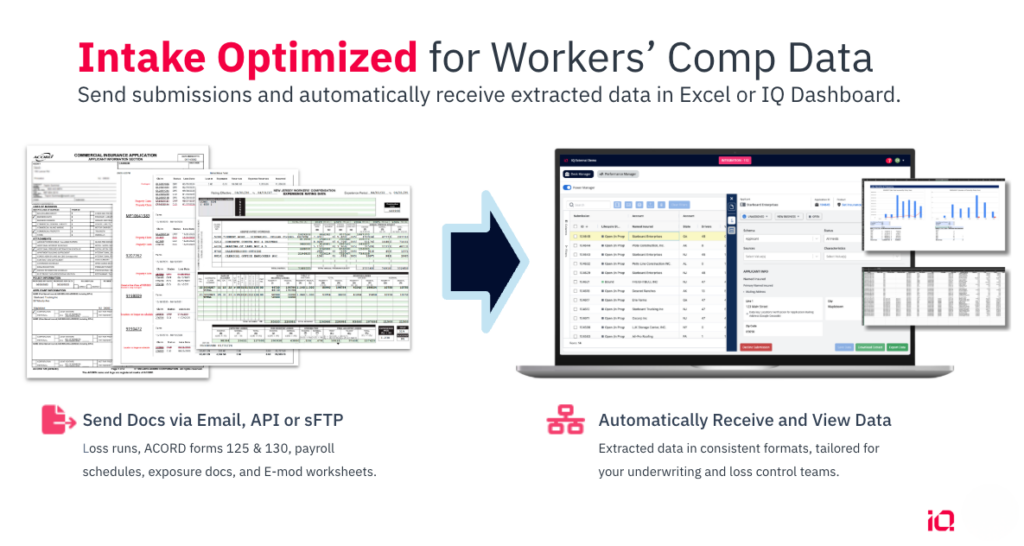

Automated Intake. Send us your workers’ compensation submissions and we handle the rest. Our intake platform automatically extracts and normalizes data from the documents your team already works with:

- ACORD forms 125 & 130

- Payroll schedules

- E-mod worksheets

- Loss runs

Data can also be enriched with third-party sources for a more complete picture of each risk. The output is structured, validated, and consistent, every time.

Submission Prep & Loss Control. Automatically receive extracted data in consistent formats, tailored for your underwriting and loss control teams. Loss Control teams leverage IQ data to identify patterns and trends within claims history. This enables more meaningful conversations with new business prospects and guides underwriting toward more informed pricing.

Workflow Integration. With that foundation in place, the right data flows directly into your existing systems, accelerating time to quote and eliminating duplicate data entry.

Workers’ Comp Intelligence. Surface priority submissions. Identify high-risk applicants early for loss control engagement. Expose buried information in loss run and exposure documents critical for risk assessment. Classify body parts and cause of injury within claims, in line with WCIO standard descriptions, and predict workers’ compensation claim subcoverages, helping distinguish between medical and indemnity, to provide forward-looking insight into claim outcomes.

Where We’d Like to Continue the Conversation

The market is healthy, the conversations are substantive, and the direction is clear: data confidence is becoming a competitive requirement, and we’re with you on that change.

We’re heading to several conferences, including: InsurTech Insights, The Future of Insurance, and ITC Vegas. We would love to connect with workers’ compensation carriers who are thinking seriously about how to build a stronger data foundation.

If that’s where your head is, let’s talk. We’d love to show you what it looks like when intake stops being a bottleneck and starts being an asset.

Continue the conversation with us. Talk with an Expert →