Every underwriting modernization effort eventually reaches the same question, and underwriting leaders tell us they wrestle with this one: do we build this underwriting technology ourselves, or do we buy it?

It sounds like a procurement question. In practice, it’s a strategic one. The answer shapes how quickly your team sees results, how much the organization spends over time, and whether the technology you deploy actually fits the way your underwriting team works.

We’ve worked through this question across more than 50 implementations with P&C carriers of varying size and complexity. What follows is the framework we use, and where we consistently see what works and what to avoid.

Build vs. buy isn’t one decision, it’s several

The reason this is hard is that build vs. buy isn’t really a single decision. It calls for different answers depending on which part of the underwriting operation you’re looking at.

The technology that drives competitive advantage (rating models, risk selection logic, proprietary data) is a fundamentally different thing from the technology that gets a submission cleanly into your systems. Treat them as the same kind of choice, and you’ll misallocate resources in both directions: over-investing where a proven vendor would do, and under-investing where your real edge lives.

Most carriers we’ve spoken with tell us about internal builds that fell short of production requirements, or vendor pilots that looked great in demo but never made it to live underwriting. That experience makes underwriting and IT teams appropriately selective. The goal is channeling that selectivity toward the right criteria for each capability, rather than defaulting to whichever option feels more familiar.

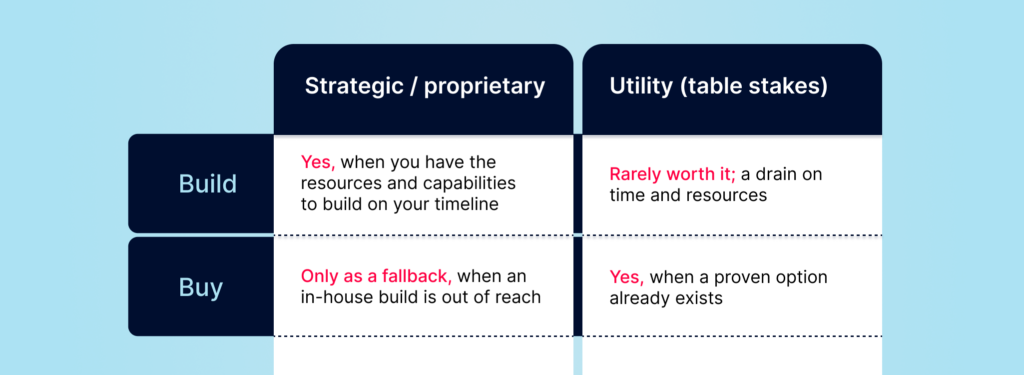

Should a P&C carrier build or buy its underwriting technology?

The short answer: build what differentiates you, buy what doesn’t, and judge both against whether a proven option actually exists in production.

That gives you two dimensions to weigh for any capability:

➔ How strategic is it? Does it shape how you select, price, or manage risk, or is it table stakes that every carrier needs and no one wins on?

➔ Is there a proven option? Can you point to a vendor running this in production today, at scale, with reference clients you can call?

Plot those two against each other and the decision gets a lot clearer:

The two corners that matter most are the ones where the answer is obvious: build the strategic capabilities that are genuinely yours, and buy the utility capabilities a proven vendor already runs well.

Which underwriting capabilities should carriers build in-house, and which should they buy?

Build: your rating and risk assessment

These are the capabilities where your expertise, data, and judgment create competitive advantage: rating algorithms, risk selection criteria, underwriting guidelines, portfolio strategy. They reflect how your organization thinks about risk, and that thinking is the one thing competitors can’t replicate.

They’re worth building and owning, even when it’s hard, because the value they create is specific to you. Rating and risk assessment is your secret sauce. The data that feeds it needs to be high quality and at your underwriters’ fingertips, but the judgment itself should stay carrier-owned.

Buy: intake and document processing

These are the capabilities every carrier needs to operate, but that look much the same across the industry: submission intake, document processing, loss run automation (turning a policyholder’s claims history into structured, usable data), data normalization. They’re table stakes. They have to work reliably and accurately, and they’re rarely where business is won.

For these, the math almost always favors buying, especially when a proven vendor already runs it in production. There’s a reason the build path is both tempting and costly here: reaching production-grade accuracy is genuinely difficult. Loss runs alone arrive in thousands of format variations; ACORD forms (the standardized applications brokers submit) are more consistent but still vary. Closing that gap takes years of training on real-world document volume. It’s infrastructure proven vendors have already built.

Where build-vs-buy decisions lose momentum

Overbuilding what a vendor already does well

The most consistent pattern we see is internal engineering pointed at capabilities where proven vendors already exist: submission intake, ACORD processing, loss run automation, workflow automation. The outcome tends to rhyme: years of effort, accuracy that stalls short of production, and the eventual realization that the problem needed more infrastructure than anyone scoped. These are exactly the table-stakes capabilities the framework above says to buy.

Under-investing in what actually differentiates

The flip side is just as costly. Every engineer assigned to a document-ingestion pipeline is one fewer building the rating models, data science, and risk intelligence that are genuinely yours. The teams that get the most from their people draw this line on purpose, and point their internal talent at the work only they can do.

Treating a pilot like proof

Many AI underwriting initiatives look sharper in a controlled demo than they do in production. Leaders tell us this is one of the most consistent gaps they’ve run into with past technology bets, which is why a strong buying process has to go beyond the proof-of-concept.

A more reliable process asks harder questions: Can the vendor show this running in production, with reference clients you can actually call? How does it handle the messy document formats you receive every day, rather than the clean ones in the demo? Can you start narrow (one line of business) and expand as the results earn it? And what does support look like after go-live? Few vendors have a real production track record, and among those that do, long-term client stability matters as much as the technology itself.

How AI is shifting the equation

It’s fair to ask whether AI changes any of this. It does make building cheaper: development cycles are shorter, iteration costs less, and internal teams have more capable tools than they used to. Over time, that should tip more capabilities toward “build.”

There’s a catch, though, and it matters more in underwriting than almost anywhere else. When an AI tool runs at roughly 60% accuracy while everyone treats its output as 100%, you get a precision gap. In underwriting, where a misclassified class code or an incomplete loss run flows straight into pricing, that gap carries real downstream cost. That same overconfidence is what quietly stalls a lot of AI initiatives. (We go deeper on what moves AI projects to production.)

So the equation is shifting, but for most carriers the destination is the same today: buying from a vendor with a demonstrated production track record gets you to results faster, and with less risk, than building from scratch.

Making the build-vs-buy call

When you’re weighing a specific capability, three questions settle most of it:

➔ Does this shape how we select, price, or manage risk? If yes, it’s strategic, worth building or customizing.

➔ Is there a vendor running this in production, at scale, with reference clients we can call? If yes, buying almost always wins on speed, accuracy, and total cost.

➔ Are we pulling engineers off strategic work to build something a vendor already provides? If yes, the math is off.

The decision itself is rarely the bottleneck. Waiting to make it is. Alignment takes time, evaluations run long, internal builds get scoped and rescoped. And while that plays out, the carriers who respond fastest are winning more business from distribution — and the gap between them and everyone else keeps growing.

The carriers who move best resolve the obvious cases first, rather than holding out for total certainty. They pick the one capability where the answer is already clear, prove value there, and let that result build the confidence and alignment for whatever comes next. It’s the same start-now-and-grow-confidently approach we’ve seen work across 50+ implementations.

Start where the case is clearest. Grow from there.

Want the full framework, including the build-vs-buy matrix and the data-first approach behind it?

Download Getting Started with AI: A Data-First Approach to see how leading P&C carriers are making these calls, the same starting point 7 of the top 15 P&C carriers have taken.

And if you’d rather talk it through for your own book, we’d love to. Let’s continue the conversation.